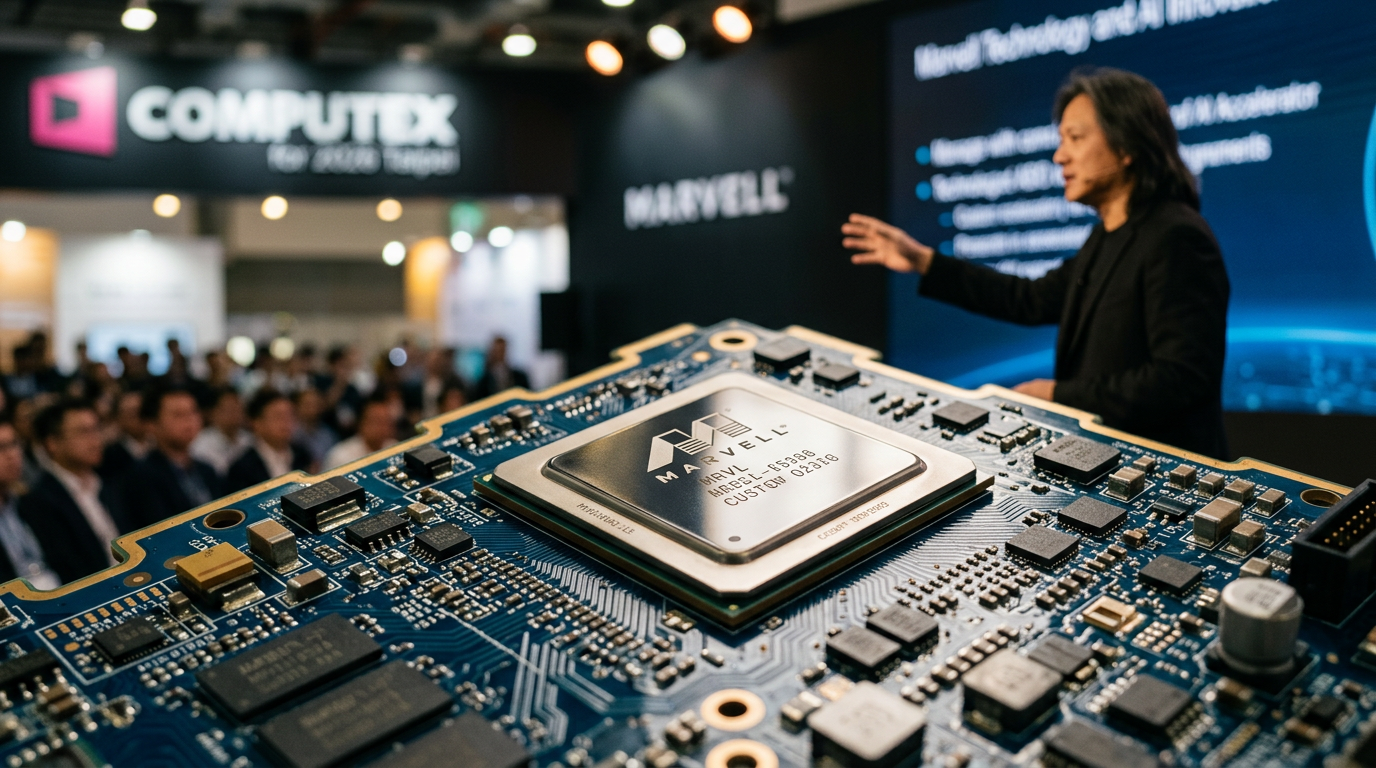

June 2, 2026. Computex in Taipei. Jensen Huang walks onstage with Marvell CEO Matt Murphy, glances at the crowd, and says four words: “The next trillion-dollar company.”

Marvell Technology (NASDAQ: MRVL) surged 32% almost instantly. Then another 10% the following morning. The market cap vaulted past $250 billion in a single session — the largest one-day gain in the company’s history.

But here’s what matters: the fundamentals were already there. Huang just pointed a spotlight at something that had been building quietly for years.

What Marvell Actually Does

Most investors think of semiconductors as GPUs and CPUs. Marvell plays a different — and arguably more critical — role. The company designs the networking and connectivity chips that allow thousands of individual processors inside a data center to communicate with each other at extreme speed. Without that glue, AI clusters don’t function.

As Huang put it at Computex: when you disaggregate a computing problem across an entire data center, what becomes essential is connectivity. That’s Marvell’s lane. And in the AI infrastructure build-out, it’s one of the most congested lanes on the road.

The company is also a leader in custom silicon — designing bespoke AI accelerators (XPUs) for hyperscalers including Amazon and Microsoft. It has 18 confirmed XPU sockets in its pipeline, and Anthropic’s massive compute expansion — anchored by a $100 billion+ commitment to Amazon Web Services — routes directly through chips Marvell designs.

The Numbers Behind the Move

The Huang endorsement wasn’t random excitement. It followed a strong Q1 fiscal 2027 earnings call on May 27, 2026, in which Marvell issued guidance that stopped a lot of analysts in their tracks.

- FY2027 revenue guidance: $11.5 billion — up roughly 40% year-over-year

- FY2028 revenue guidance: $16.5 billion — another 45% step-up

- Interconnect revenue: expected to rise 70%, raised from prior guidance of 50%

Microsoft’s North American data centers currently source 100% of their optical chips from Marvell. The company also recently acquired Polariton Technologies, a silicon photonics firm, adding deep expertise in next-generation optical platforms.

One analyst’s near-term price target sits at $400 — roughly 30% upside from post-Computex levels — with a longer-range case of $650 to $700 if the company gets re-rated on par with Broadcom.

Where the Risk Lives

It would be incomplete to skip the uncomfortable part. The stock trades at roughly 85x forward earnings post-rally — well above the semiconductor sector average of 35x. That’s a premium that leaves no margin for a miss.

There’s also the Anthropic IPO wildcard. If that listing is delayed or scaled back, the pace of infrastructure commitments could slow, directly affecting Marvell’s order cadence. And while Huang’s endorsement carries enormous weight, it is ultimately a prediction — not a contract.

Insiders have been net sellers over the past 12 months, which is worth noting without over-interpreting.

Why This Matters Right Now

Citigroup just raised its year-end 2026 S&P 500 target to 8,100, citing what it called an “unprecedented” AI capex super-cycle. Four out of six major thematic equity baskets are outperforming the broader market in 2026, with AI and robotics leading the pack.

Marvell sits at the intersection of two of the most durable forces in that cycle: custom silicon demand from hyperscalers and the connectivity infrastructure required to run frontier AI models. Those tailwinds don’t hinge on any single product launch or partnership — they’re structural.

The question isn’t whether Marvell belongs in the conversation. It does. The question is whether the entry point still makes sense after a 150%-plus run — and whether the Street’s growth estimates, which now call for $16.5 billion in fiscal 2028 revenue, are conservative or already baked in.

Worth a close look before the next earnings catalyst resets the narrative entirely.